When businesses grow, decisions become more complex and the risks increase. Leaders like directors and officers play a vital role in guiding companies, but their choices sometimes lead to legal trouble—even if they act in good faith. Directors and Officers (D&O) insurance helps shield these key people from personal loss if they are sued over actions taken while managing a company. For both large corporations and small businesses, understanding D&O coverage is essential to protect leadership and attract top talent. This article explains what D&O insurance is, what it covers, who needs it, and how it works, so you can decide if it’s right for your organization.

What Is Directors And Officers Insurance?

Directors and Officers insurance is a liability policy made to protect a company’s decision-makers. If a director or officer faces a lawsuit for alleged wrongful acts while managing the organization, D&O insurance can help cover legal costs, settlements, or judgments. These wrongful acts might include errors, misleading statements, neglect, or breach of duty. Importantly, D&O insurance protects the individual’s personal assets, not just the company’s money.

Many people confuse D&O insurance with other business policies. Unlike general liability or professional liability insurance, D&O is focused on risks faced by those in leadership positions. It fills a unique gap, especially as lawsuits against company leaders are becoming more common—even in private companies and nonprofits.

Why Is D&o Insurance Important?

Personal Liability For Leaders

One of the biggest surprises for new directors or officers is that they can be held personally liable for their actions. This means their house, savings, or even retirement funds could be at risk if they are sued. D&O insurance provides a financial safety net, making it easier to attract qualified people to leadership roles.

Rising Claims And Legal Costs

Lawsuits against directors and officers are on the rise. According to a 2022 survey by Chubb, over 25% of private companies reported a D&O claim in the past three years, with average claim costs exceeding $400,000. Even if a claim is groundless, defending it can be expensive and time-consuming.

Investor And Stakeholder Expectations

Investors, lenders, and board members often require D&O coverage before joining or funding a company. Having a solid D&O policy sends a message that the company values good governance and risk management.

Regulatory Demands

Companies in highly regulated industries—like finance, healthcare, or education—face extra scrutiny from government agencies. D&O insurance helps leaders navigate these risks without fear of personal ruin.

What Does D&o Insurance Cover?

D&O insurance is not a one-size-fits-all policy. Coverage can vary, but most policies share some core protections. Here’s what is typically included:

Common Covered Claims

- Breach of fiduciary duty (e.g., mismanaging company funds)

- Misrepresentation of company assets or performance

- Errors in judgment or poor decisions

- Employment practices claims (e.g., wrongful termination, discrimination)

- Failure to comply with laws or regulations

- Shareholder actions (e.g., claims of unfair treatment or lost value)

- Creditor or vendor disputes

Real-world Example

A company’s board decides to merge with another business. Some shareholders believe the merger was unfair and sue the directors for allegedly failing to get the best deal. Even if the board acted in the company’s best interest, legal fees can add up.

D&O insurance steps in to pay for defense and, if needed, settlements.

What’s Not Covered

D&O insurance does not cover:

- Fraud or criminal acts (if proven in court)

- Personal profits gained illegally

- Bodily injury or property damage

- Claims covered under other policies (like general liability)

- Legal action between directors within the same company

Understanding what’s excluded is as important as knowing what’s covered.

Who Needs D&o Insurance?

Many people think only big public companies need D&O coverage, but the reality is broader.

Public Companies

Stock-listed companies face lawsuits from shareholders, regulators, and even competitors. D&O insurance is a must-have for these organizations.

Private Companies

While private businesses may not have public shareholders, they still face risks from employees, creditors, and partners. Lawsuits for mismanagement or employment issues are common.

Nonprofits

Directors of nonprofits can be sued for wrongful acts just like those in for-profit businesses. Volunteers and board members want protection before they serve.

Startups And Small Businesses

Early-stage businesses often overlook D&O insurance. However, as soon as you raise outside funding, hire employees, or form a board, D&O coverage becomes important.

Credit: commercial.allianz.com

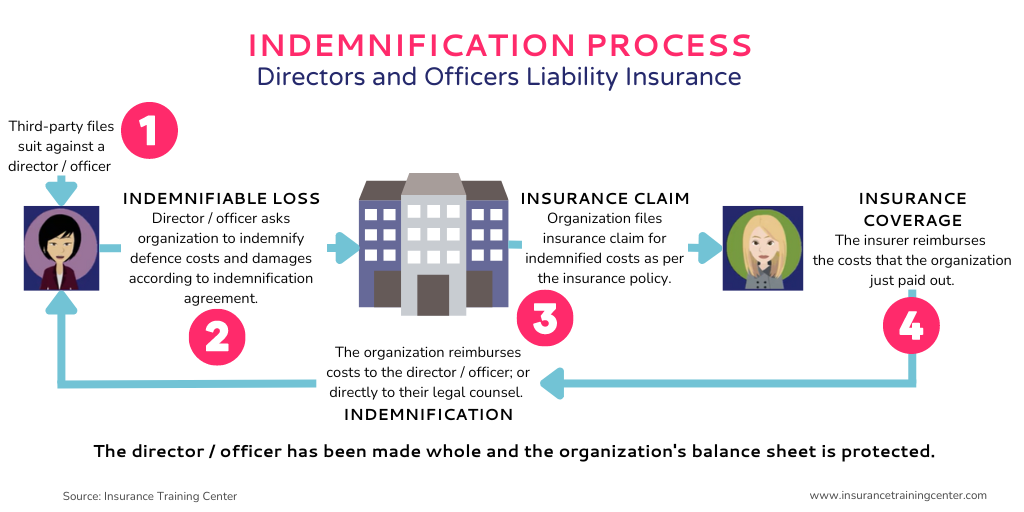

How Does D&o Insurance Work?

D&O policies are “claims-made” insurance. This means the policy only covers claims made while the policy is active, not before or after.

The Three Sides Of D&o

Most D&O policies include three main coverage parts, often called “sides”:

| Coverage Side | What It Protects | Who Gets Paid |

|---|---|---|

| Side A | Directors and officers (when company can’t pay) | Individual leaders |

| Side B | Company (for indemnifying directors/officers) | The company |

| Side C | Company (for claims against the company itself) | The company |

Side A is most crucial when a company is bankrupt or legally barred from helping its leaders.

Claims Process

When a covered claim happens, the company or director notifies the insurer. The insurer then investigates and, if covered, pays for defense costs, settlements, or judgments up to the policy limits. It’s vital to report claims promptly—waiting too long can lead to denial.

Deductibles And Limits

D&O policies have deductibles (the amount you pay before insurance kicks in) and coverage limits (the maximum the insurer will pay). Choose limits carefully, based on your company’s size and risk.

Key Factors When Choosing D&o Insurance

Not all D&O policies are the same. Here are the most important things to look for:

- Coverage scope: Does the policy protect against all likely risks, including employment practices or cyber liability?

- Policy limits: How much will the insurer pay per claim and in total? Too little coverage can leave you exposed.

- Exclusions: Understand what’s not covered, such as prior acts or certain lawsuits.

- Defense costs: Are these included within the policy limits or in addition to them? This can affect how much is left to pay settlements.

- Retroactive and extended reporting periods: Can you add coverage for past actions or claims made after the policy ends?

- Reputation of insurer: Choose a financially strong insurer with experience in D&O claims.

D&o Insurance Cost Comparison

Here’s a snapshot of D&O insurance premium ranges by company type:

| Company Type | Annual Revenue | Estimated Annual Premium |

|---|---|---|

| Small Private | <$5 million | $2,000 – $5,000 |

| Medium Private | $5–50 million | $5,000 – $15,000 |

| Large Public | >$50 million | $25,000 – $100,000+ |

| Nonprofit | Any | $800 – $3,000 |

Premiums depend on many factors, including claims history, industry, and desired limits.

Credit: insurancetrainingcenter.com

Common Mistakes When Buying D&o Insurance

Many companies make avoidable errors when getting D&O coverage:

- Assuming you don’t need it: Even small or family-run businesses can face lawsuits.

- Choosing the cheapest policy: Low price often means weaker coverage or more exclusions.

- Not reading the policy details: Always review exclusions, definitions, and limits.

- Ignoring “tail” coverage: If you sell the company or change insurers, you may need coverage for claims made later.

- Forgetting entity coverage: Make sure the policy covers claims against the company, not just individuals.

- Underestimating defense costs: Legal fees can quickly use up limits—plan accordingly.

A non-obvious insight: Many claims are not dramatic fraud cases but simple HR complaints or procedural mistakes. Also, D&O policies can cover costs for investigations, not just lawsuits.

D&o Insurance Vs. Other Business Policies

D&O is only one part of a business’s risk management plan. Here’s how it compares to other coverage:

| Policy Type | Main Purpose | Who/What Is Protected |

|---|---|---|

| D&O Insurance | Management liability | Directors, officers, company |

| General Liability | Physical injury/property damage | Company (third-party harm) |

| Professional Liability (E&O) | Errors in services | Company/professionals |

| Employment Practices Liability (EPLI) | Workplace disputes | Company, management |

Some policies, like EPLI, may be bundled with D&O. But always check for gaps.

How To Get The Most From Your D&o Policy

Maximize your protection by:

- Reviewing your policy yearly, especially after big changes like mergers or new investors.

- Training your board and leaders on risk and compliance.

- Keeping good records of all board decisions and meetings.

- Reporting potential claims to your insurer quickly.

- Working with a knowledgeable broker or advisor familiar with your industry.

- Considering extra coverage (“excess” D&O) if you’re in a high-risk sector.

A tip many miss: D&O policies are negotiable. Ask your broker if you can remove exclusions or add protections for your unique risks.

The Future Of D&o Insurance

Lawsuits against directors and officers are becoming more frequent and costly. Issues like cyber breaches, #MeToo claims, and global regulations are adding new challenges. Insurers are responding with more tailored policies and higher premiums, especially for tech, healthcare, and financial companies.

In the coming years, expect to see more focus on ESG (environmental, social, and governance) risks. Boards should stay updated on emerging threats and review their D&O coverage often.

For more in-depth industry data and trends, you can visit the official resource at IRMI: Directors and Officers Liability Insurance.

Credit: allenthomasgroup.com

Frequently Asked Questions

What Is The Main Purpose Of D&o Insurance?

The main purpose is to protect directors and officers from personal financial loss if they are sued for actions taken while managing a company. It covers legal costs, settlements, and sometimes investigation expenses.

Does D&o Insurance Cover Criminal Acts?

No, D&O insurance does not cover proven criminal acts, fraud, or illegal personal profits. It only covers wrongful acts done in the course of normal company management.

Is D&o Insurance Needed For Small Or Family Businesses?

Yes, even small or family-run companies can face lawsuits from employees, creditors, or partners. D&O insurance protects leaders regardless of business size.

How Much Does D&o Insurance Cost?

Costs vary widely by company size, industry, and coverage limits. Small businesses might pay $2,000–$5,000 a year, while large public firms can pay $100,000 or more.

What Is “tail” Coverage In D&o Insurance?

Tail coverage (also called extended reporting period) lets you report claims made after the policy ends, for actions taken during the coverage period. It’s important after mergers, acquisitions, or leadership changes.

As business risks evolve, having the right D&O insurance isn’t just smart—it’s essential. By understanding how this coverage works and what to look for, you can protect your leaders and your organization’s future.

Read More:

- Condo Insurance Policy Comparison: Find the Best Coverage Fast

- Professional Liability Insurance Coverage: What You Need to Know

- Best Home Insurance Discounts 2026: Unlock Big Savings Now

- Indexed Universal Life Insurance Plans: Smart Wealth Protection

- Expat Health Insurance Coverage: What You Need to Know Now

- High Net Worth Insurance Providers: Secure Your Wealth Today

- Insurance SEO Services for Agencies: Boost Rankings & Leads

- Insurance Claim Settlement Process: Step-by-Step Guide to Success