The insurance claim settlement process is often seen as confusing and slow, especially for beginners. You may hear stories of delayed payouts, rejected claims, or endless paperwork. But understanding this process can help you avoid mistakes and get your money faster.

Whether you are dealing with health, car, property, or life insurance, knowing how claims are settled gives you real control and peace of mind.

This article explains the insurance claim settlement process step by step. You’ll learn about the main stages, what documents are needed, how companies decide payouts, and how to handle disputes. We’ll use simple language, clear examples, and practical advice. By the end, you’ll know what to expect, how to make the process smoother, and what rights you have as a policyholder.

What Is An Insurance Claim?

An insurance claim is a request made to an insurance company for compensation after a loss or damage covered by your policy. For example, after a car accident, you file a claim to get your repair costs paid. In health insurance, you submit bills for hospital treatment. Claims can be for money, repairs, or replacement of lost items.

Not all claims are accepted. Insurers check your policy, the facts of the case, and other details before deciding. If the claim fits the policy rules, you’ll get compensation. If not, your claim may be rejected or reduced.

Key Steps In The Insurance Claim Settlement Process

Understanding the steps helps you avoid delays and mistakes. Here’s a clear breakdown of the claim settlement process:

1. Notification Of Loss

As soon as a loss happens, inform your insurer. Most companies require prompt notice—usually within 24 to 48 hours for car or property damage. Delaying this step can lead to rejection.

2. Filling Out Claim Forms

You need to complete a claim form. This includes details about the incident, your policy number, and your contact information. Forms are usually available online or at the insurer’s office.

3. Providing Supporting Documents

Submit documents such as police reports (for theft or accident), hospital bills, repair estimates, photos of damage, and proof of ownership. Missing documents are a common reason for delays.

4. Claim Assessment And Investigation

The insurer reviews your claim. For simple cases, this may take a few days. For bigger claims, like fire or major accidents, they might send a surveyor or investigator.

5. Approval Or Rejection

If your claim fits the policy terms, it’s approved. If not, it’s rejected with a clear reason. Sometimes, the company may offer a reduced amount.

6. Settlement And Payment

Once approved, the insurer pays you, repairs your property, or covers the medical bills. Payment times vary—some claims are settled in days, others take weeks.

Typical Timeline For Claims

| Claim Type | Average Settlement Time | Common Delays |

|---|---|---|

| Health Insurance | 7-14 days | Missing medical bills, unclear diagnosis |

| Car Insurance | 10-30 days | Police report delay, incomplete forms |

| Property Insurance | 15-45 days | Surveyor visit, value disputes |

| Life Insurance | 10-60 days | Document verification, nominee issues |

Required Documents For Claim Settlement

Documents are essential for claim approval. Here are the common documents for each type:

- Health Insurance: Hospital bills, doctor prescriptions, diagnosis reports, insurance card, discharge summary.

- Car Insurance: Police FIR, driving license, registration certificate, repair bills, photos of accident.

- Property Insurance: Proof of ownership, police report (for theft), photos, repair estimates.

- Life Insurance: Death certificate, policy document, nominee’s ID, medical records (if needed).

Tip: Keep copies of all documents. Submit them in a single batch to avoid back-and-forth requests.

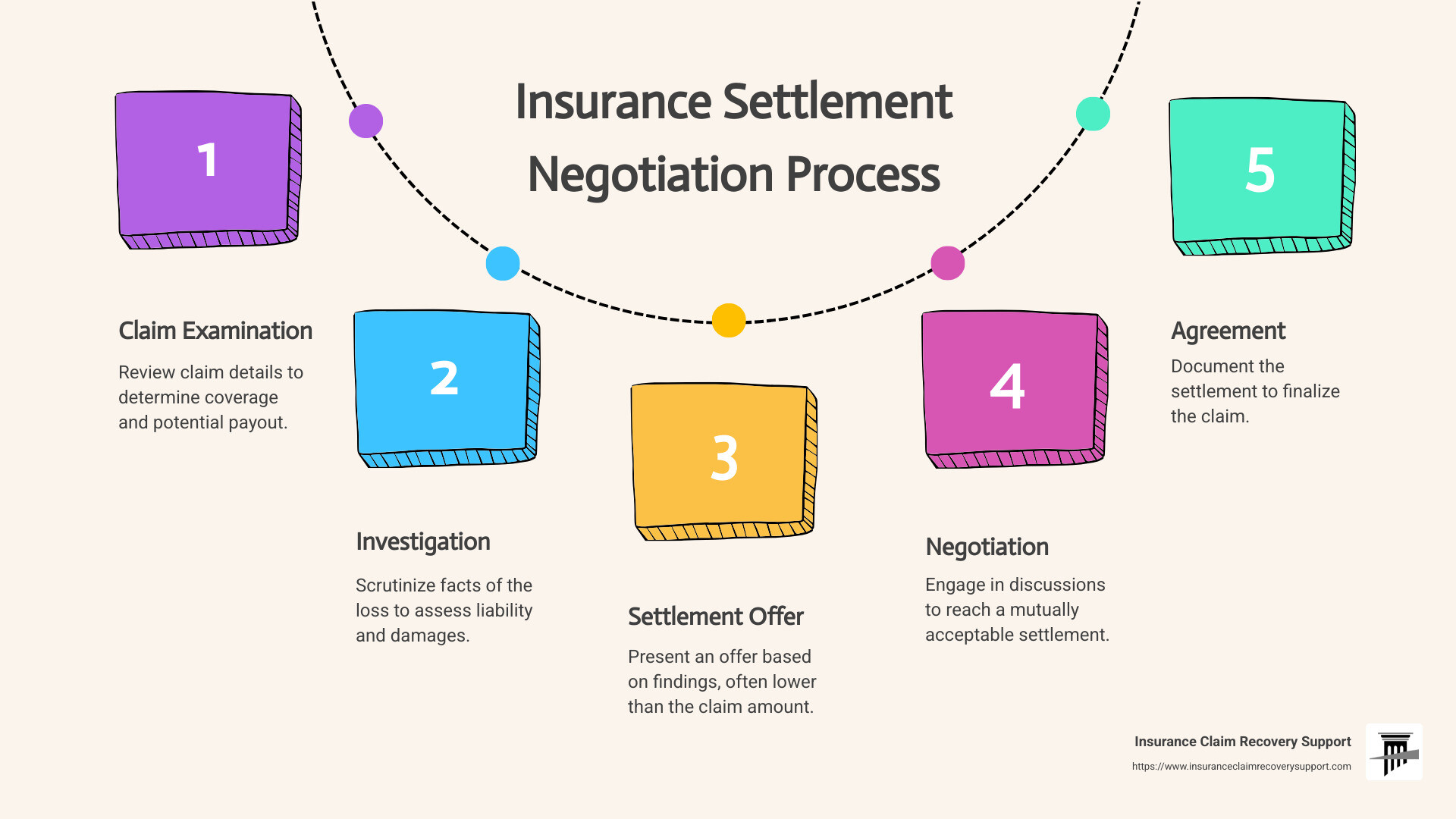

How Insurers Evaluate And Settle Claims

Insurance companies follow strict rules to assess claims. Here’s how they decide:

Claim Investigation

For big claims, insurers may appoint an investigator or surveyor. Their job is to:

- Check if the claim matches the policy terms.

- Assess the value of loss or damage.

- Identify any fraud or misrepresentation.

Surveyors may visit your property, interview witnesses, or request extra documents.

Claim Calculation

Insurers use formulas to decide payouts. For example:

- Health Insurance: Covers actual medical expenses, minus deductibles or co-payments.

- Car Insurance: Pays repair costs, minus depreciation or excess.

- Property Insurance: Pays for repair or replacement, minus wear and tear.

Here’s a sample comparison of payout calculations:

| Claim Type | Claim Amount Requested | Deductibles/Excess | Payout |

|---|---|---|---|

| Health Insurance | $5,000 | $500 | $4,500 |

| Car Insurance | $7,000 | $1,000 | $6,000 |

| Property Insurance | $15,000 | $2,000 | $13,000 |

Common Reasons For Claim Rejection

Insurers reject claims for several reasons:

- Non-disclosure: Not revealing important facts when buying the policy.

- Policy exclusions: Losses not covered by the policy (like intentional damage).

- Fraud: False claims or forged documents.

- Delayed claim: Not informing the insurer quickly.

- Incomplete documents: Missing or unclear paperwork.

Insurers must explain the rejection in writing. You can appeal or provide more details.

Credit: www.slideteam.net

Tips To Speed Up Your Insurance Claim

Many claims are delayed due to small mistakes. Here’s how to get faster settlements:

- Read your policy carefully. Know what is covered and what is not.

- Notify your insurer quickly. Delays can lead to rejection.

- Collect all documents early. Don’t wait for the company to request them.

- Follow up regularly. Ask for claim status updates every week.

- Be honest and clear. Give accurate details—don’t exaggerate or hide facts.

- Keep records. Save emails, claim numbers, and conversation notes.

Insight: Some insurers offer online claim tracking. Use these tools to check progress and avoid phone delays.

Settlement Methods: Cashless Vs Reimbursement

Insurance claims are settled in two main ways:

Cashless Settlement

You don’t pay upfront. The insurer pays the hospital or repair shop directly. This is common in health and car insurance.

- Advantage: Less paperwork, faster service.

- Limitation: Only at approved network providers.

Reimbursement Settlement

You pay first, then claim your money back. You must submit bills, receipts, and proof.

- Advantage: Flexibility to choose any provider.

- Limitation: Slower process, more paperwork.

Here’s a comparison of both methods:

| Settlement Method | Process | Time Taken | Documents Needed |

|---|---|---|---|

| Cashless | Direct payment to provider | 1-3 days | Minimal |

| Reimbursement | Claim after payment | 7-30 days | All bills & receipts |

Credit: insuranceclaimrecoverysupport.com

Handling Disputes And Complaints

If your claim is delayed or rejected unfairly, you have rights. Here’s what to do:

- Ask for written explanation. Insurers must explain their decision.

- Appeal the decision. Submit more documents or clarify facts.

- Contact the regulator. In the US, contact your state insurance department.

- File a complaint. Use online portals or write a formal letter.

Non-obvious insight: Many disputes are resolved by simply providing missing documents or clarifying facts. Don’t rush to legal action—try direct negotiation first.

For more information, check the official National Association of Insurance Commissioners consumer resources.

Non-obvious Insights For Beginners

- Policy wording matters: A single word can change your coverage. For example, “accidental damage” may not cover “wear and tear.” Always ask your insurer to explain unclear terms.

- Nominee mistakes: In life insurance, wrong nominee details can delay payouts for months. Check and update nominee information every year.

- Digital tools: Many insurers now offer claim apps. These speed up document submission and status checks.

Credit: www.crossml.com

Frequently Asked Questions

What Happens If I Miss The Claim Notification Deadline?

Most insurers have strict deadlines for reporting a loss. If you miss it, your claim can be rejected. Some companies allow late claims for genuine reasons—like hospitalization or travel—but you must provide proof. Always notify your insurer as soon as possible.

Can I Claim If The Loss Is Less Than My Deductible?

No. The deductible is the amount you pay before the insurer covers the rest. If your loss is less than the deductible, you won’t get a payout. For example, if your car damage is $300 and your deductible is $500, you pay all costs yourself.

What Should I Do If My Claim Is Rejected?

First, ask for a written explanation. Review your policy to see if the rejection is valid. If you think it’s unfair, appeal with extra documents or clarification. You can also contact your state insurance regulator or consumer forum.

Is It Possible To Get A Partial Settlement?

Yes. Sometimes, insurers approve part of your claim if only some losses are covered, or if documents are incomplete. For example, if you submit bills for $5,000 but only $3,000 fits the policy, you’ll get a partial payout.

How Long Does The Claim Settlement Process Take?

The time depends on claim type, amount, and paperwork. Health and small car claims are settled in days; property and life insurance may take weeks or months. Missing documents and investigation can increase delays. Always ask your insurer for an estimated timeline.

Navigating the insurance claim settlement process can feel overwhelming, but with the right knowledge and preparation, you can make it much smoother. Understand your policy, keep your documents ready, notify your insurer quickly, and follow up regularly. Most disputes happen due to missing information or unclear communication, not because insurers want to avoid payment.

By following these steps and tips, you can avoid common mistakes and get your claim settled efficiently. Remember, you have rights as a policyholder—use them wisely and stay informed for a stress-free experience.

Read More:

- Condo Insurance Policy Comparison: Find the Best Coverage Fast

- Directors And Officers Insurance Coverage: Essential Protection Guide

- Professional Liability Insurance Coverage: What You Need to Know

- Best Home Insurance Discounts 2026: Unlock Big Savings Now

- Indexed Universal Life Insurance Plans: Smart Wealth Protection

- Expat Health Insurance Coverage: What You Need to Know Now

- High Net Worth Insurance Providers: Secure Your Wealth Today

- Insurance SEO Services for Agencies: Boost Rankings & Leads