Choosing the right life insurance can feel overwhelming, especially when you’re comparing term life insurance and whole life insurance. Both offer protection for your loved ones, but they work in very different ways. If you’re unsure which is best for you, this guide will help you understand the differences, costs, and real-life examples, so you can make a confident decision.

What Is Term Life Insurance?

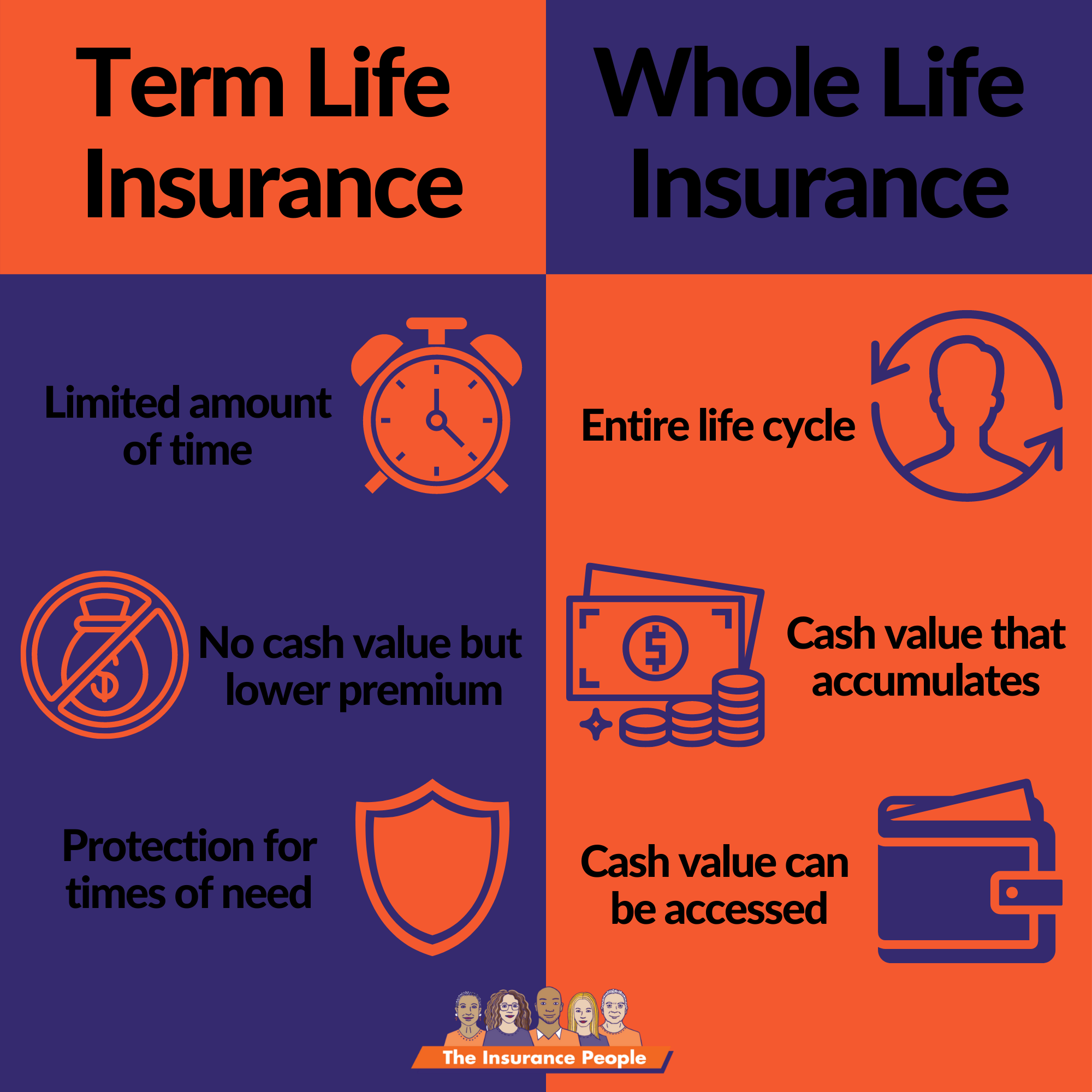

Term life insurance is a simple policy that covers you for a set period, like 10, 20, or 30 years. If you die within that time, your family gets a lump sum of money called the death benefit. If you’re still alive when the term ends, the policy stops, and you get nothing back.

Most people choose term life because it’s affordable and easy to understand. It’s popular with young families, people with loans or mortgages, and anyone who needs coverage for a specific time.

Key Features

- Coverage period: Usually 10–30 years

- Premiums: Fixed and lower than whole life

- Death benefit: Paid only if you die during the term

- No cash value: You don’t build savings with this policy

For example, a 35-year-old non-smoker might pay about $25 per month for a $500,000, 20-year term policy. That’s much less than a whole life policy with the same coverage.

Pros And Cons

Advantages:

- Low cost: It’s much cheaper than whole life.

- Simple: Easy to apply and understand.

- Flexible: Choose the term that fits your needs.

Disadvantages:

- Temporary coverage: It ends after the term.

- No savings: You can’t withdraw money.

- Premiums can rise: If you renew after the term, costs go up.

What Is Whole Life Insurance?

Whole life insurance is a permanent policy. It stays active your entire life, as long as you pay the premiums. Besides the death benefit, it also has a cash value feature. Part of your premium goes into a savings account that grows over time.

Key Features

- Lifetime coverage: No expiration, covers you for life

- Premiums: Fixed but much higher than term

- Death benefit: Paid whenever you die

- Cash value: Builds up and can be borrowed or withdrawn

For example, a 35-year-old non-smoker might pay about $400 per month for a $500,000 whole life policy. The cash value grows slowly, but you can borrow against it after a few years.

Pros And Cons

Advantages:

- Permanent protection: Your family is always covered.

- Savings feature: Builds cash value you can use.

- Fixed premiums: Costs stay the same for life.

Disadvantages:

- High cost: Much more expensive than term.

- Complexity: More rules and details.

- Slow growth: Cash value builds slowly, especially in early years.

Term Life Vs Whole Life: How They Compare

To help you see the differences clearly, here’s a side-by-side comparison.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Coverage Duration | 10–30 years | Lifetime |

| Premiums | Low and fixed | High and fixed |

| Cash Value | None | Yes, builds over time |

| Death Benefit | Only if you die during term | Guaranteed, whenever you die |

| Policy Loans | No | Yes, from cash value |

| Renewal Options | May be renewed, often at higher rates | Not needed (permanent) |

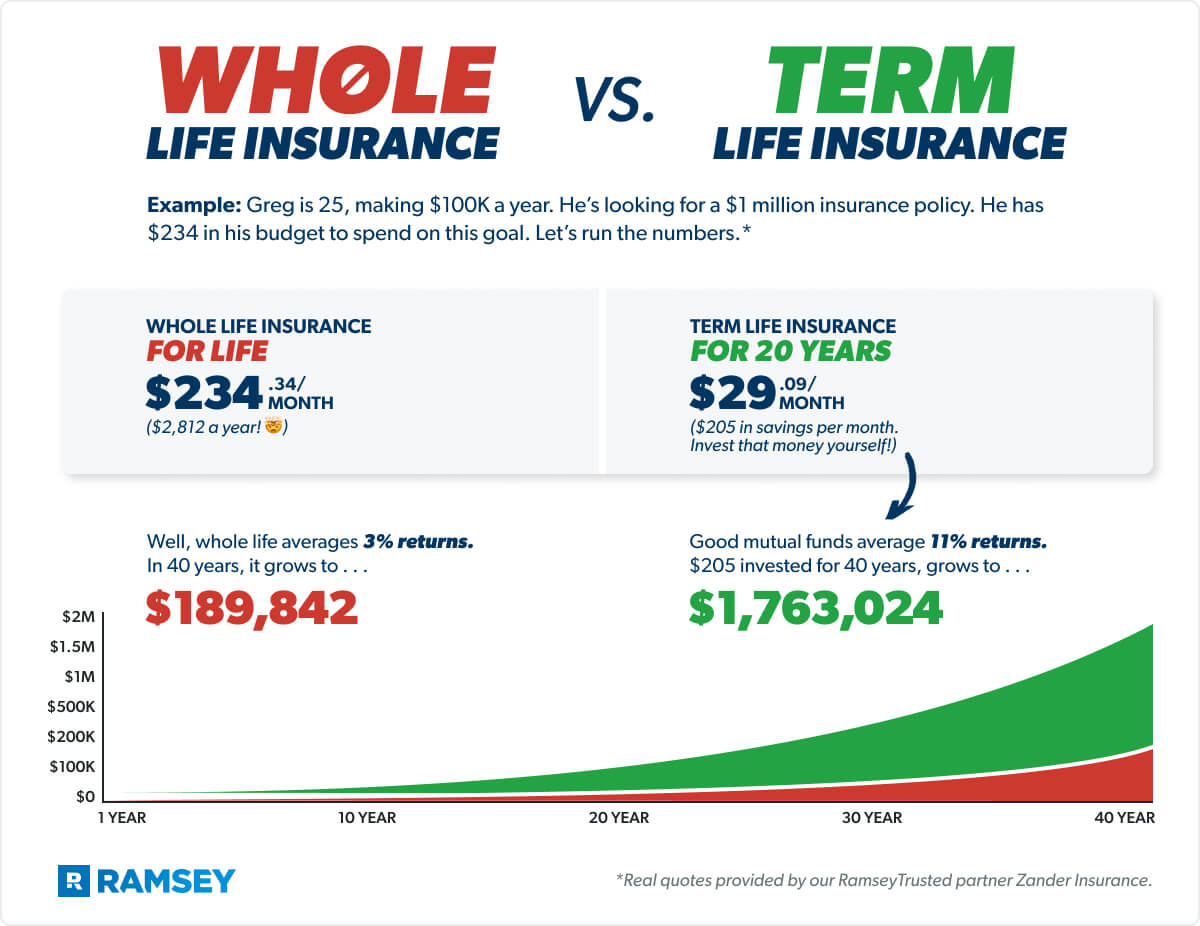

Cost Comparison: Real Numbers

Price is often the biggest difference. Let’s look at the costs for a healthy 35-year-old, non-smoker seeking $500,000 in coverage.

| Policy Type | Monthly Premium | Annual Premium | Cash Value after 10 years |

|---|---|---|---|

| Term Life (20 years) | $25 | $300 | $0 |

| Whole Life | $400 | $4,800 | ~$8,000 |

Term life is much cheaper, but you don’t get any savings. Whole life costs more, but part of the premium goes into cash value, which grows slowly.

Who Should Choose Term Life Insurance?

Term life is best for people who:

- Need coverage for a limited time (until kids grow up, mortgage paid)

- Want low-cost protection

- Are starting families or buying homes

- Prefer simple policies without extra features

If you’re focused on protecting your family until your debts are paid, or your children become independent, term life makes sense. You can get high coverage for a low price, then drop the policy once your needs change.

Non-obvious Insight: Laddering Policies

Many people don’t realize they can buy multiple term policies with different lengths. For example, buy a 10-year policy to cover a car loan, and a 20-year policy for your mortgage. This way, your coverage matches your changing needs, and you don’t overpay.

Who Should Choose Whole Life Insurance?

Whole life suits people who:

- Want lifelong coverage

- Like the idea of building cash value

- Want to leave a legacy or pay estate taxes

- Have complex financial needs

If you want insurance that never expires and like the savings feature, whole life is a good option. It’s popular with people planning for retirement, high-net-worth families, or those who want to help pay funeral costs and debts.

Non-obvious Insight: Policy Loans

One overlooked benefit is policy loans. You can borrow against your cash value for emergencies or big expenses. The money is yours to use, but interest applies. If you don’t pay back, it reduces your death benefit.

Credit: www.insuranceppl.com

Common Mistakes When Choosing Life Insurance

- Focusing only on price: Cheap premiums might not cover all your needs.

- Ignoring health changes: If you wait until you’re older or sick, premiums rise.

- Over-insuring: Buying more coverage than you need wastes money.

- Assuming one policy fits all: Your needs may change, so review policies regularly.

- Forgetting about inflation: $100,000 may sound like a lot now, but will it be enough in 20 years?

How Cash Value Works In Whole Life Insurance

The cash value grows slowly, but it’s guaranteed. Part of each premium goes into savings, which earns interest. After a few years, you can borrow or withdraw money. Some people use it for emergencies, college tuition, or extra retirement income.

| Year | Cash Value (Typical) | Available for Loan |

|---|---|---|

| 5 | $3,000 | $2,700 |

| 10 | $8,000 | $7,200 |

| 20 | $22,000 | $19,800 |

Cash value is not the same as investment returns. It’s slow, steady growth. If you cancel your policy, you can get the cash value back, but fees may apply.

Real-life Example: Family Protection

Let’s say Sarah, age 40, has two kids and a mortgage. She buys a 20-year term life policy for $500,000 at $30 per month. If she dies within 20 years, her family gets $500,000 to pay bills and cover expenses.

Sarah’s friend, Mark, buys a whole life policy for the same amount. He pays $450 per month, but his policy builds cash value. Years later, Mark borrows $10,000 from his cash value to help his daughter with college costs. His policy stays active, but his death benefit drops by $10,000 unless he pays it back.

Which Is Better For Your Needs?

There’s no one-size-fits-all answer. Here’s how to decide:

- If you need affordable coverage for a fixed time, choose term life.

- If you want permanent protection and savings, choose whole life.

- If you’re unsure, start with term life. You can convert to whole life later with some policies.

Most financial experts recommend term life for most people, especially if you’re young or have debts. Whole life is best for those with long-term goals or who value the savings feature.

If you want more details or personalized advice, check trusted resources like the Investopedia guide on life insurance.

Credit: funeraladvantage.com

Frequently Asked Questions

What Happens If I Outlive My Term Life Insurance?

If you outlive the term, your coverage ends. You don’t get any money back. Some companies offer return of premium options, but they cost more.

Can I Convert Term Life To Whole Life?

Many term policies allow conversion to whole life, often before age 65. This lets you get permanent coverage without a new health check.

Is Whole Life Insurance A Good Investment?

Whole life is not a traditional investment. The cash value grows slowly and is guaranteed, but it’s best for people who want lifelong protection and savings.

How Much Life Insurance Do I Need?

A common rule is 10–15 times your yearly income. Consider debts, family needs, and future expenses. Don’t just pick a number—think about what your family would need.

Are Premiums Tax Deductible?

For most people, life insurance premiums are not tax deductible. However, the death benefit is usually tax-free for your beneficiaries.

Final Thoughts

Choosing between term life insurance and whole life insurance depends on your goals, budget, and family situation. Term life gives you affordable, flexible protection for a set period. Whole life offers permanent coverage and slow-growing savings. Both have unique advantages—and risks—so it’s smart to compare, ask questions, and review your needs often. Remember, the right policy is the one that fits your life, not just your wallet.

Credit: www.ramseysolutions.com

Read More:

- Condo Insurance Policy Comparison: Find the Best Coverage Fast

- Directors And Officers Insurance Coverage: Essential Protection Guide

- Professional Liability Insurance Coverage: What You Need to Know

- Best Home Insurance Discounts 2026: Unlock Big Savings Now

- Indexed Universal Life Insurance Plans: Smart Wealth Protection

- Expat Health Insurance Coverage: What You Need to Know Now

- High Net Worth Insurance Providers: Secure Your Wealth Today

- Insurance SEO Services for Agencies: Boost Rankings & Leads